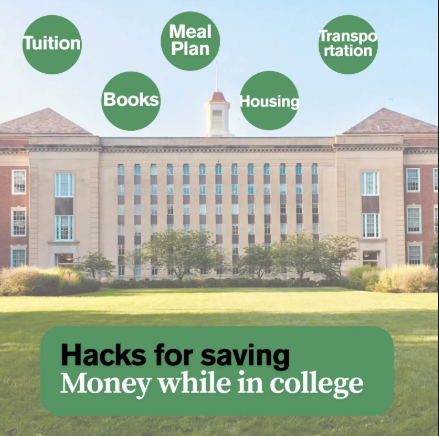

In today’s world, a college education is a gateway to earning better job opportunities and long-term stability. However, the cost of college is continuously rising, so to be that successful person, families and students need to start saving as early as possible.

Over the past couple of decades, college tuition has risen significantly. According to the College Board, the average cost of tuition and fees at public four-year schools is over $10,000, not including things like housing, transportation, food, and books, which can be overwhelming for college students.

Additionally, it is difficult to make money in college, so lots of students depend on loans which brings unwanted debt for many years after graduation. It can take anywhere from years to decades to repay. Saving money in advance will help students in their adult lives with less financial stress and more freedom and help the parents by also reducing their stress because they’re not worrying as much about where they’re going to get that money for college from.

Saving early also gives students more options about where they want to go. It prevents them from limiting their options based on cost and more based on what best fits their interests. Another benefit is that it reduces the likelihood of having to work long hours to provide for yourself.

Although the financial aspect of college can seem intimidating, saving little by little can be an effective practice in saving your money; a little goes a long way. A 529 plan, for example, is a great way to start the process of saving and can grow significantly by the time students are ready to apply for college.

Ultimately, saving for college is about saving and investing in your future. It is a way for families to show support to their children, for students to take ownership of their education, and for both parties to ease the burden of college fees and rising costs. The earlier planning begins, the more doors open and the smoother your path to success will be.